“This Time Is Different”… Again

Every so often, something surfaces that rattles investors’ and our financial news media confidence. A crisis, a conflict, a change in policy. It almost always arrives wrapped in the same seductive phrase: “This time it’s different.”

We heard it in 2016 with Brexit.

In 2018, it was trade war rhetoric—culminating in a Christmas Eve when the market was down 25%.

In early 2020, we endured the swiftest 30% market decline in history—followed almost immediately by the fastest recovery ever recorded.

Then came 2022, with the highest inflation in 40 years and the most aggressive interest rate hikes since the 1980s.

And now, in 2025, tariffs have once again taken center stage—evoking comparisons to the protectionist policies of the 1930s, and even further back to President McKinley’s platform of the 1890s.

So here we are again. Different headlines. Same Reaction

Let’s remind ourselves: Wall Street—and the companies it represents—do not care who the president is. Markets have advanced under Democrats and Republicans, through wars, scandals, crises, and recoveries. What matters most is not who sits in the White House, but whether you remain seated in your financial plan.

If we’ve learned anything from the past century of market history, it’s this: circumstances change, but average investor behavior stays the same. Panic. Recovery. Growth. Repeat.

Now—and this is essential—the enduring 10%+ average annual return of the equity market and its frequent, temporary declines are not two unrelated phenomena. They are part of one indivisible whole. The volatility is not just normal; it is necessary. It is the emotional toll we pay for participating in the long-term wealth-creating miracle of capitalism.

Please understand: I do not believe you are the average investor. What I am saying is this: volatility is part of the journey. We planned for it, it's been part of every client review I have conducted. We expect it.

A Case in Point: April 7th

On April 7th, the market opened down 2%. Then, on the strength of a rumor—a potential 90-day delay in newly announced tariffs—the market surged 8%. Moments later, when the rumor was denied, the gains disappeared just as quickly. Nearly $2.4 trillion in market value evaporated in the space of a few hours, all driven by speculation.

I mentioned in our April 3rd email to clients "Market recoveries often happen swiftly, and missing just a handful of the best days can significantly reduce long-term returns" And then, as if to underline the point: on April 9th, the 90 day delay was officially confirmed. The market responded with another sudden move—this time up 9%—even as long-term questions about trade policy remained unresolved.

This is not investing. This is emotional voting, fueled by headlines and hearsay. This is what markets do in the short term—they fluctuate, sometimes violently, based on narrative and noise.

But over time, markets stop voting and start weighing. They weigh earnings, innovation, productivity, and progress. And those who remain invested in that process—not just through the quiet stretches, but through the storms—are the ones who capture the long-term rewards.

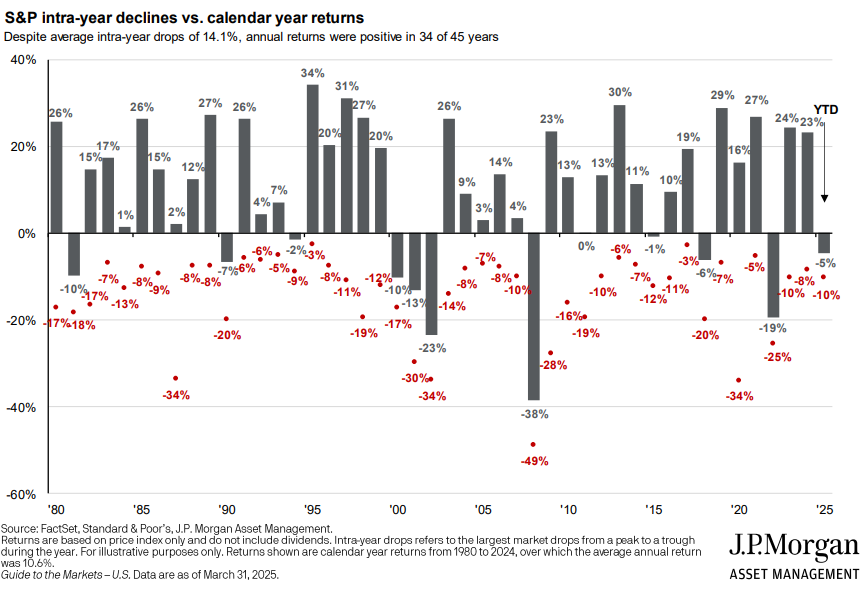

The market’s premium return has always been the compensation for enduring this volatility. The declines are not just inevitable—they are indispensable. You cannot have one without the other. (Just look at the S&P 500’s intra-year declines compared to its annual returns graph below.)

So no, we will not attempt to time the market. We will not allow momentary fear to dictate lifelong decisions. We will stay the course—because every time we have done so in the past, we’ve been rewarded with what this journey is ultimately about: peace of mind, prosperity, and progress.

Taxes, Taxes and you guessed it... Taxes!

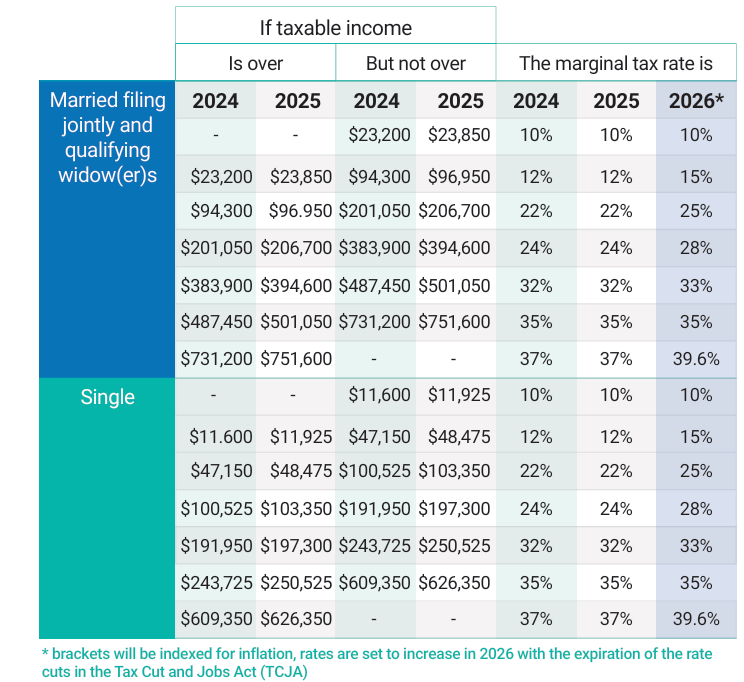

One of the most significant tax laws in recent history—the Tax Cuts and Jobs Act (TCJA)—is set to expire at the end of 2025. This means that, barring new legislation, many of the tax benefits individuals and families have enjoyed since 2018 will disappear, and higher tax rates will return.

If nothing changes, income tax brackets are set to rise, the standard deduction will shrink, and key deductions will be altered. In short, many Americans will see their tax bills increase. The question isn’t if taxes are going up—it’s by how much.

What This Means for You

For those in higher tax brackets, this could mean thousands of dollars in additional taxes owed each year. Business owners, retirees, and high-income earners may be particularly affected by the reversal of lower rates and deductions. Estate tax exemptions are also scheduled to be cut in half, making proactive planning even more essential.

While tax laws are always subject to change, waiting until the last minute is not a strategy. Now is the time to take a proactive approach and assess how these changes could impact your financial future.

What You Should Do Now

The first step is to understand your current tax situation. Please send us a copy of your most recent tax return so we can evaluate how these changes may affect you and identify strategies to mitigate the impact. You can send it to us via our website https://www.theharborwealth.com/clients -> send us a document, send it via email to Ellen, ellenv@harborw.com , or request a FedEx envelope to send us a physical copy.

Whether it’s accelerating income, making strategic Roth conversions, or revisiting estate planning, there are steps you can take now to prepare for the future.

Need Something Notarized?

Our Client Relationship Manager, Ellen, Is in the process of becoming notary!

Give us a call and we'll happily notarize what you need!

Mark Your calendar!

- Elliott will be having a webinar with Collen Ceh Becvar, Owner of Trinity Advocacy Group and Gernotologist In June. The discussion will focus on how to plan for care as we age, how to find care, what the best kind of planning entails and when to start. Their website is

https://trinityadvocacygroup.com

Please submit any questions to hello@harborw.com beforehand! - Shred Event and Food truck on August 12!

We hope everyone has a great start to the spring!

Graham is excited for warm weather!.